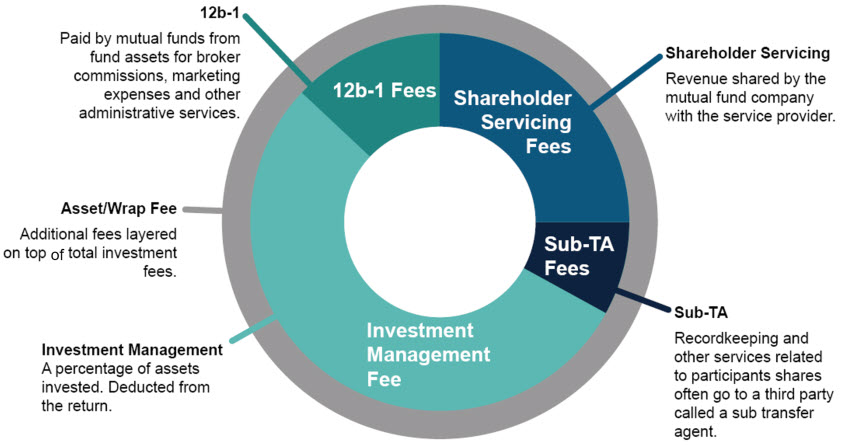

Retirement plan fees are complicated. Between administration, investment management, recordkeeping, consulting, revenue sharing, sub-TA and 12b-1, it isn’t always clear to plan participants or plan sponsors exactly what they’re paying, how much they’re paying or even who’s paying the fees.

ERISA Section 408(b)(2) states that plan fiduciaries have to determine whether the agreements and compensation of service providers are “reasonable.” The rule requires service providers to supply plans with disclosures to help them determine if fees are “reasonable.” Financial network Limited helps fiduciaries with this complicated determination by identifying:

- All of the total plan cost components

- The various primary drivers of retirement plan pricing

- The role of revenue sharing

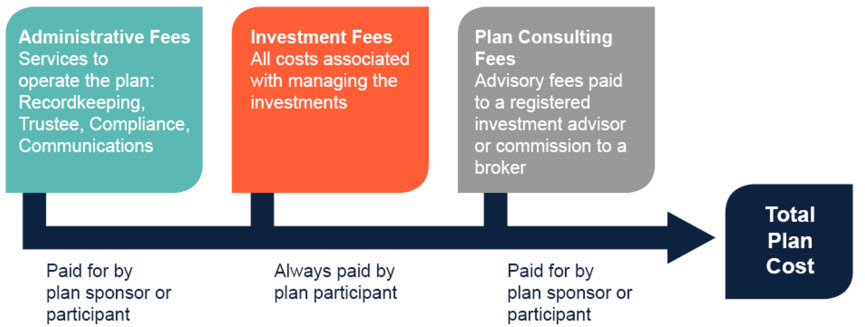

Cost Components

The three main components are administrative fees, investment fees and plan consulting fees. Administrative and plan consulting fees may be paid by the plan sponsor or the participant. Investment fees are always paid by participants and deducted from plan assets.